-

Dave,

Q1: I have a question regarding after entering into a successful primary robot trade. One can never be faulted for taking money off the table along the way. Its a personal preference, right?

A1: Absolutely. Statistically, scaling in on new signals is less optimal than scaling out. Its a hard decision to make, especially by how much, 25%, 33%, 50%? And you may decide to re-enter the sold portion on new daily entry price limits. If I can understand the psychological comfort that such decisions can bring, you are bound for some good instant gratifications trades in a mean-reversion environment (40% of the time) and for many frustrating opportunity losses in a trending environment (60% of the time).

Q2: The recent trade on TZA, which was stopped out at close to a nice 5% profit, showed unrealized profits of over double that along the way. I believe this was true of a previous robot trade. It appears to me much as there are optimal entry points; there are also optimal exit points, to take at least some profits off the table.

A2: The last 2 trades were victims of mean-reversion and have been stopped out. Being stopped out, even with profits on a trailing stop, is the least optimal of all exits. But the one and only optimal exit point for the robot is to exit on a 20 DMF signal change after a lasting and trending trade. These are the ones we try to catch and ride fully invested because thats where the bulk of the risk-adjusted performance is coming from. You may use robot statistics to evaluate good or satisfactory scaling-out levels, but they are far from optimal.

Q3: I understand the larger picture is to remain in the trade and the market could have just as easily rolled over and we would be deep in the money at this point.

A3: Thats exactly my thesis.

Q4: I think you have made reference to intermediate exit points along the way giving probabilities, but I didnt quite understand. Given how the robot seems so accomplished at picking an entry point, would it not be very good at picking an intermediate exit point? For those of us that perhaps would like to reduce their position size and take some profits off the table. Maybe this is clear to everyone given the LT ST information, but not to me.

A4: I never made reference to intermediate exit points, but to most probable 3-day targets for monitoring the evolution of a trade. Such targets can be discretionarily used as exit points, but they are not exit targets in my view. Quite to the contrary, hitting these targets within 3 days tells you that the trade is evolving perfectly as expected. If probabilities remain positive from that point, you certainly dont want to exit as a big trend-following run may be just around the corner.

The LT/ST information on the robot page is always based on projections from the last CLOSING price. For Tuesday, it says: In the past this combination led to a 3D short LOSS of -0.11% from the previous day's close. The trade became positive after three days in 53.1% of the cases. If you were in a winning trade with such statistics, would you really have an advantage taking some money off the table to avoid a 3-day loss of -0.11% while having more than 50% chance of increasing your profit in the same 3-day period?

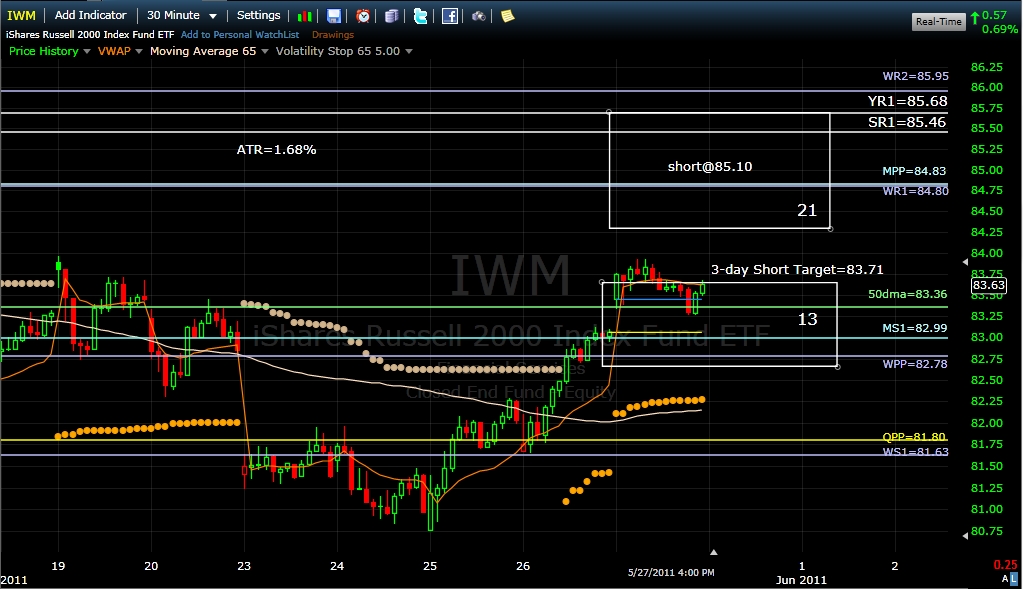

Q5: Perhaps its old age, but I seem to be getting lost in the probabilities of all this. If you could just explain the edge in terms of probabilities for Tuesdays trade, that might help me understand. Its a primary robot trade, but the short settings are neutral. The short settings are neutral at last close of 83.65 which would lead to a 3D loss? If the trade is triggered at 85.10, do we know from the past what the 3D gain or loss would be? If IWM rallies hard and approaches 86.86 stop level, do we know anything about the probabilities? Perhaps all of this could be explained in term of: If one had traded X dollars for the last robot primary trade, would you be allocating the same X dollars for this trade?

A5: You must absolutely distinguish between the ST/LT statistics from the previous close (83.65) and the expected gain and probabilities if entering a new position at the limit entry price (85.10).

For Tuesday, the most probable 3-day target from the CLOSE is a rise of 0.11% with only 46.9% chances (because there are 53.1% odds that the price will be lower) or :

83.65 + (83.65* 0.11% * 46.9%) = 83.693. This very neutral indeed.

But the most probable 3-day target if you have the opportunity to enter at the limit entry price of 85.10 is:

85.10 (85.10 * 2.64%* 61.67%) = 83.71

This is pretty close to the previous target of 83.69. The main difference for the robots trading account is that it will not miss shorting a bounce to 85.10 in-between. If IWM never trades at or above 85.10 during open market hours, the robot will simply wait and stay in cash.

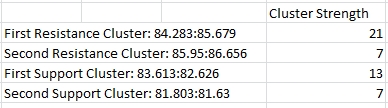

Here are the clusters and their strengths for Tuesday. Notice that the new monthly pivots starting on Wednesday will somehow improve the support cluster strengths if Tuesdays close is higher or unchanged from Fridays close.

Posting Permissions

Posting Permissions

- You may not post new threads

- You may not post replies

- You may not post attachments

- You may not edit your posts

Forum Rules

Reply With Quote

Reply With Quote