-

05/12/2013 Mousetrap

Sector Model XLB 3.97%

Large Portfolio Date Return Days

BBRY 7/16/2012 114.34% 299

SEAC 9/25/2012 34.03% 228

CAJ 9/25/2012 2.73% 228

BOKF 2/4/2013 15.72% 96

SWM 2/12/2013 21.11% 88

MWW 4/11/2013 18.30% 30

ABX 4/11/2013 -14.64% 30

TPX 4/22/2013 5.65% 19

NYCB 4/24/2013 1.43% 17

TTM 5/6/2013 4.96% 5

S&P Annualized 10.50%

Sector Model Annualized 26.40%

Large Portfolio Annualized 34.97%

From: http://market-mousetrap.blogspot.com...e-trading.html

Rotation: selling SEAC; buying DLB.

This is an odd rotation. Both are in the same industry, but the fundamental configuration of DLB is better positioned to take advantage of the technical aspects of the model. This doesnt happen that often. I think in the past two years this has only happened one other time.

Now back to time frames

Weve seen how we can use an analysis of past years to estimate the next few quarters, and an analysis of previous decades to estimate the next few years.

Today Im going to look at something to AVOID: using an analysis of multiple decades to estimate the next quarter. Thats using too big a dataset for too small a time frame.

Weve all heard the Keynes quip that the markets can stay irrational longer than you can stay solvent. He was likely speaking to just such a mistake. Even the tiniest of variances can break your investment tolerances if you look at a time frame too big for your model.

To give an example, think of a coin toss. Lets say that you win on heads and lose on tails. Over the course of time there should be about the same number of heads as there are tails. The operative word here is about. There should be ABOUT the same number of heads as tails.

ABOUT is not the same thing as EXACTLY.

Most of us will shrug our shoulders and plow ahead anyway. How bad can it be?

Lets look at a 5% variance (normal for this kind of exercise). At 100 tosses, thats only 5. At 1000, 50. At 10,000, its 500.

To make matters worse, that 5% is just a typical variance. Some folks might see no variance at all and others might see 10% or more.

Try making a gambling system that will make you money and still be 500 times off from where you think it should be. Youll break your pocket before you break the bank.

Now, lets keep this in mind when we think of very long term macro-economic indicators.

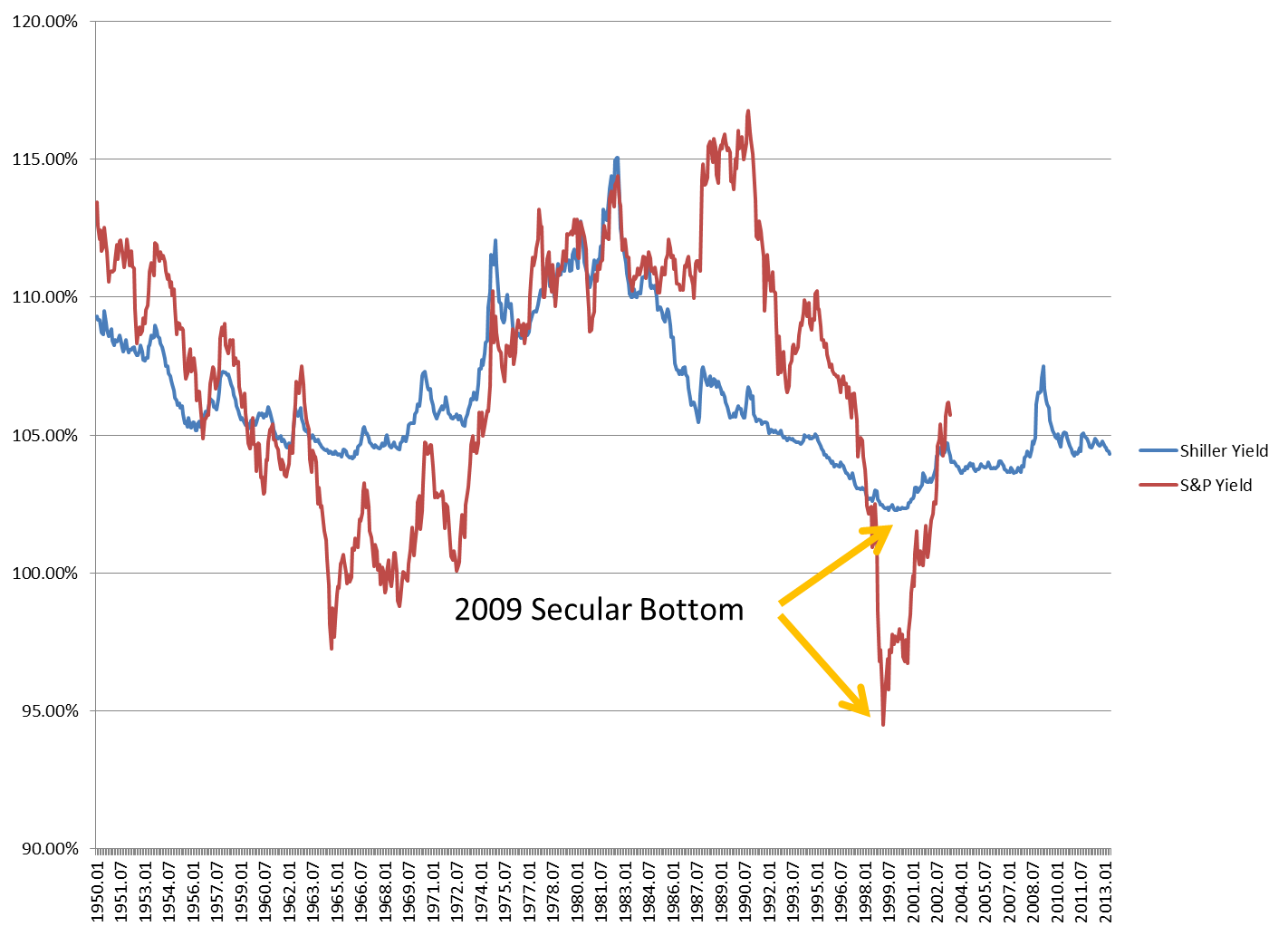

Well start with what I call the Shiller Yield.

The Cyclically Adjusted P/E ratio invented by Shiller can be easily converted into a Cyclically Adjusted Earnings Yield:

To create this, I added two columns to the spreadsheet available from Shiller at http://www.econ.yale.edu/~shiller/data.htm . The two columns are a 10 year earnings yield (i.e. the Shiller Yield) and the ACTUAL 10 year yield of the S&P from the listed date forward (called S&P Yield).

Earnings Yield is just the inverse of a Price to Earnings ratio.

Even though the S&P is more volatile, the average monthly variance between the projected Shiller and actual S&P yields is only 2.78%. As a wise old friend used to say, thats close enough for government work.

The problem is, HOW to use it.

That 1999 to 2009 bottom is pretty clear on the graph.

But it would be inappropriate to use that tiny hiccup on the 2013 projection (from 2003) to try to anticipate a correction in 2013. We might have one, but trying to TIME a short term move based on a tiny blip in a ten year smoothed average is something no one should ever try to do.

Such a projection is highly irresponsible for two reasons: first, the S&P sometimes disconnects for years from the Shiller Yield; and second, in this age of competitive quantitative easing, no one can even estimate what a correction would look like.

So who would make such a mistake?

Check out: http://www.hussman.com/wmc/wmc130513.htm

Youll see something similar to my Shiller Yield on that article.

Now, I LIKE Hussman a lot. But Im going to pick on him here. Hussman is usually spot on with his decade long analysis. His explanations of the present liquidity trap Bernanke has put himself into are quite insightful.

But Hussman makes the mistake of trying to use these ten year analyses to estimate the next quarter.

Even worse is the simple fact that there is a problem with the Shiller Yield that can never be properly adjusted for: the Shiller Yield is never negative, not in its entire 150 year history. Even at the 1929 top, the Shiller Yield was still above 102%.

If you use the Shiller Yield, youll always be long and I mean, ALWAYS.

Hussman isnt always long. In fact hes been very heavily hedged for most of this 2009 to present bull run-up.

So, he uses a very long term indicator thats always long to figure out when to go

short?

And he argues that Bernanke is trapped in QE and then invests as if Bernanke

isnt?

Right

Hussman is too clever by half. He knows the limitations of his indicators and still tries to do one better, and he ends up being left behind.

So HOW does one use a Shiller Yield? Remember, its never short (at least not in the United States).

But the United States is not the only regional market.

One could review ALL of the cyclically adjusted (i.e. Shiller) yields for the various regions and to invest in the ones with the lowest CAPE ratio. Theres a more complete explanation of that idea here:

http://etfdb.com/2013/going-global-e...nts-with-cape/

But even that has risk, because at the greatest extremes its not impossible for a region to have a complete collapse. One investor I know did quite well investing in a Greek ETF based on the CAPE ratio. It was a good call, and well played. But what if Greece had actually collapsed? It DOES happen on occasion, and you only need to be wrong once to ruin your day.

So, CAPE trading isnt a primary strategy for the bulk of your funds. Its a supplement, at best as long as you can exercise EXTREME patience

CAPE trading is something a person does over a lifetime. Its a strategy to buy and hold, and hold, and hold, and hold, and hold. If, for instance, a person were putting a little away for retirement each month, the key is to put that months investment into the region with the lowest CAPE ratio (or in the graph above, the highest Shiller Yield), and THEN NEVER SELL IT, EVER, until you need it in retirement.

Over the course of your lifetime your investments will be spread out in different global regions and well diversified, with no tax burden at all until a portion is used during retirement.

Its a good strategy if you cant use an IRA and you dont want to worry about stock selection, market timing, or taxes.

And even though global markets tend to be more unified than they were in the past, there are still laggards.

Although I am looking at optimizing after-tax net profits, this is further than I plan to go myself. But it IS an interesting approach, and potentially the longest term a person can do. Anything longer term than this would fall under another one of Keynes famous quips: In the long run, were all dead.

Tim

Posting Permissions

Posting Permissions

- You may not post new threads

- You may not post replies

- You may not post attachments

- You may not edit your posts

Forum Rules

Reply With Quote

Reply With Quote